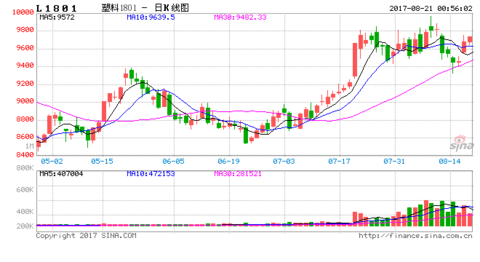

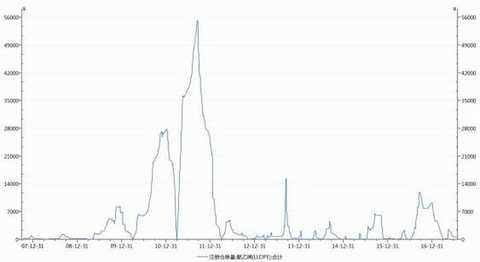

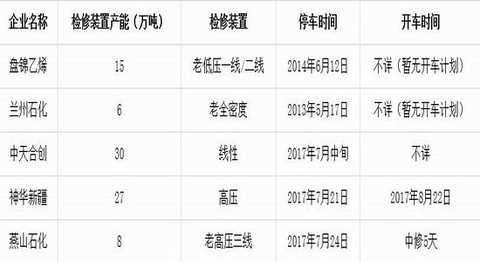

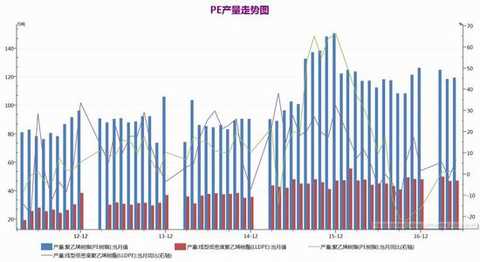

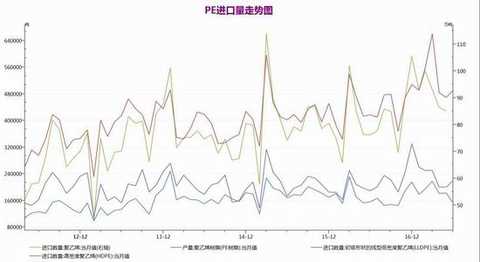

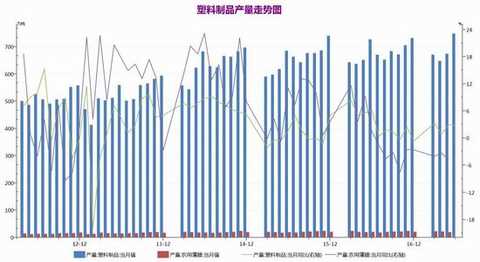

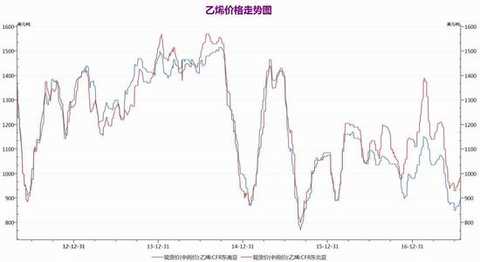

Hot spot funds flow to thousands of stocks to evaluate stocks to diagnose the latest rating simulation transaction Client Registration : The annual banking festival “2017 China Banking Development Forum and the 5th Bank Comprehensive Selection Awards Ceremony†hosted by Sina Finance will be held on August 24th at the Westin Beijing Financial Street Hotel, so stay tuned . [registration entry] At the beginning of July, the market did not affect the expected increase in market outlook and demand, and the price fluctuated. Afterwards, the supply of the market continued to decrease and the original strength, the domestic policy of prohibiting the import of waste plastics, etc., the price volatility surged to a high near 9750. At the end of the month, the price of the downstream water spot is not high, and the demand for high-priced raw materials is not high, and the price of the package is not affected. In August, the market supply pressure increased, coupled with the slow start of the downstream demand season, supply and demand allocation, the expected price futures shock adjustment, the central line continued to strengthen. First, the analysis of fundamental factors (1) Analysis of supply and demand 1, short-term inventory pressure is not big Judging from the domestic inventory statistics of Zhuo Chuang.com, the overall social stock of PE has continued to fall slightly since March, because the inventory of PE is composed of social inventory, port inventory and petrochemical inventory. Port inventory: The market trend was good in July, the port was out of the warehouse, the port inventory continued to decline; the petrochemical side, the market trading atmosphere is good, coupled with the lower operating rate in North China, the petrochemical inventories continued to decline; traders, 7 The monthly price fluctuated higher. In the early stage of the market, the stocks were low in the market with weak market conditions. Under the sentiment of buying and not buying, the downstream purchasing enthusiasm increased, and the traders' inventory continued to decline. In the aftermarket, petrochemical inventories may rebound slowly due to the rebound in operating rates and the increase in import sources. figure 1. Inventory data Source: Zhuo Chuang Information figure 2. Warehouse receipt data Source: Wande Information 2. Equipment capacity and maintenance In the first half of the year, the new capacity equipment was put into operation and there were Surbana Enterprises and Zhongtian Hechuang. Jiangsu Surbana is a methanol-to-olefin process. This unit produces EVA. Zhongtian Hechuang is put into operation on a high-pressure 250,000-ton/year plant, and another set is expected to be put into operation in the second half of the year. Shenhua Ning coal, which was originally planned to be put into operation in June, was postponed to the second half of the year with a total capacity of 430,000 tons/year. Zhongtian Hechuang's 12 tons/year high pressure has not yet been opened. The market outlook focuses on Shenhua Ningmei, Zhongtian Hechuang and Zhonghai Shell. It is expected that the new capacity production will have limited impact on August. In terms of overhaul of PE equipment: In August, the maintenance of equipment was greatly reduced. In addition to the long-term parking of Panjin Ethylene and Lanzhou Petrochemical, only Zhongtian Hechuang and Shenhua Xinjiang were in the inspection period in August, affecting the output of about 40,000 tons. image 3. New capacity production plan Figure 4. Device maintenance plan Source: Longzhong Petrochemical 3. Production According to Zhuo Chuang Information, domestic PE production in June 2017 was approximately 1,165,600 tons, with a cumulative total output of 7.608 million tons. In June 2017, production decreased by 5.95% from May and decreased by 1.89% year-on-year. The output of LLDPE is 490,500 tons, the output of LDPE is 221,500 tons, and the output of HDPE is 453,500 tons. The operating rate of the unit rebounded from July to August, and the output is expected to increase compared with the previous period. Figure 5. PE production chart Source: Wande Information 4. Import and export According to customs statistics, the total export volume of PE in June 2017 was 22,864.77 tons. The export volume of LLDPE was 4721.6 tons, and the export volume increased by 84.68% compared with the previous month. The average export price of the month was 1516.1 US dollars/ton; the export volume of HDPE was 12491.43 tons, and the export volume decreased by 15.82% compared with the previous month. The average export price of the month was 132.86 US dollars/ The export volume of LDPE was 5,561.74 tons, and the export volume increased by 9.45% compared with the previous month. The average export price of the month was 1,466.92 US dollars/ton. In June 2017, PE imports amounted to 864,800 tons, an increase of 1.55% from the previous month and an increase of 13.4% from the same period last year. The total import volume was 5.641 million tons, an increase of 17.42% year-on-year. Among them, the import volume of LLDPE was 221,000 tons; the import volume of HDPE was 491,400 tons; the import volume of LDPE was 152,400 tons, mainly due to the large linear and high-pressure imports, and the export price was mainly due to the drop in domestic prices and the foreign price. Figure 6. PE import and export chart Source: Wande Information 5, demand analysis In June 2017, China's plastic products increased by 18.16% year-on-year. Plastic film production increased by 4.9% year-on-year; agricultural film decreased by 4.9% year-on-year. At present, the packaging film and HDPE monofilament have higher opening power, and rise to more than 60%, and the agricultural film operating rate is at 24%. Mainly affected by environmental inspection, the downstream small-scale product factory was closed due to unqualified inspection, and the downstream agricultural film operating rate was worse than that of previous years. At present, the operating rate of large manufacturers is maintained at 2-4%, and the agricultural film industry enters the reserve stage in July-August. The start of construction was slightly better than the previous period. However, the market volatility is fierce, the terminal procurement enthusiasm is not high, and the quantity of raw materials purchased is determined according to the order. Figure 7. Plastic product chart Source: Wande Information (2) Cost analysis From the statistics of Longzhong Petrochemical's statistical cost, the oil profit is around 2,500 yuan/ton, and the coal-based PE profit is around 3,300. The overall upstream factory profits are relatively rich. Figure 8. Cost profit chart Source: Longzhong Petrochemical (III) Analysis of upstream raw materials Recently, due to the peak summer travel season in the United States, gasoline and diesel inventories fell and the Saudi energy minister said that OPEC may further reduce production. The United Arab Emirates and Nigeria also have favorable factors such as the willingness to reduce production, and the oil price fluctuated. In terms of market outlook, OPEC's supply still shows signs of increase. US crude oil production and the number of drilling platforms continue to increase, and supply pressure is difficult to ease. On the demand side, the US summer is still at the peak of travel, and crude oil inventories are still expected to continue to be digested. Become the main positive support in the near future. The Fed’s interest rate hike is expected to cool down, and the dollar’s ​​recent performance is sluggish, which is also good for oil prices. Although the OPEC meeting did not restrict Libya and Nigeria's immunity, Nigeria has expressed its support for production cuts. Saudi Arabia and the United Arab Emirates have even pushed down production expectations and released a positive signal. Recent favorable factors prevail, and oil prices are expected to remain strong and volatile. On July 28th, the closing price of ethylene was at US$990/ton CFR Northeast Asia and US$905/ton CFR Southeast Asia. The price was higher than that in June. The upstream crude oil cost support and most of the downstream equipment maintenance were restarted. The demand was boosted and the ethylene price was expected. It is showing a stable and small rise pattern. Figure 9. Ethylene price chart Source: Wande Information (4) Basis In view of the current price difference, we select the price difference between the active contract of plastics and the spot price of Tianjin in North China to predict the possible trend of the two markets. As of July 28, 2017, the current price of LLDPE is up to RMB 75/ton. In the middle and late period, the domestic market price has risen sharply under the ban on the import of waste plastics. The spot price of the premium is more than 300, and then the downstream is resistant to high-priced raw materials. Larger, limit prices continue to rise momentum, futures prices weaken, and repair the basis. From the domestic and international price difference, as of July 28, the domestic and international price difference is about 75 yuan / ton, the domestic price quickly rises after the spot. In the early period, domestic prices weakened and discounted foreign prices, and imports fell sharply. However, as domestic prices rose, ports and imports would continue to increase. Figure 9. Spread chart Source: Ruida Futures (5) Technical analysis From the weekly chart, the main contract of L is now down to the middle of the Bollinger Band. The MACD forms a golden fork. From the perspective of quantity, the short-term lightening down, the trading volume has not been enlarged, and the market is expected to have limited downside. space. Below focus on the support near 9000, the pressure around the 9800 test, short-term fallback adjustment, it is recommended to take a bargain-hunting strategy. For arbitrage, the L1801-1805 contract can be gradually arbitrarily arranged in the -100-0 range. (6) Summary of opinions In summary, the upstream crude oil is coming to support during the peak season of gasoline demand in summer, and it is expected to maintain a strong shock and support the cost of polyethylene. On the supply side, although the initial equipment maintenance has been fully resumed, the market supply has gradually increased, but the short-term overall PE inventory remains relatively The low level, while the new expansion capacity is limited, and the returning market is affected by environmental inspections and customs bans on foreign garbage operations, the demand for new materials is expected to increase, and the supply pressure in the market is expected to be small. However, on the demand side, the downstream small and medium-sized unqualified products enterprises were closed due to environmental inspections, and the demand was slightly worse than in previous years, but there were signs of improvement in the previous months. And downstream in the early stage of the weak market, the terminal is not stocking. In August, the fundamentals were intertwined, but in September, gold, nine silver and ten, there is a certain demand for stocking. It is expected that plastics will show a trend in August. In operation, take a bargain-hunting strategy. Second, the operation strategy and risk tips (1) Operation strategy 1, unilateral operation strategy (1) Position cost: The transaction adopts a batch-building strategy, and the position cost is controlled at 9,000 yuan/ton. (2) Risk control: If the futures price is 8800 yuan/ton, the partial stop loss will be executed. If the closing price of the futures price is below 8,700 yuan/ton, Then you need to stop loss processing for all positions. (3) Position period: The position of this transaction is 1 month, and the market conditions are adjusted according to changes in market conditions. (4) Take Profit Plan: The current price will run in our strategic direction. The top position will be gradually built around 9000. The upper target will look at RMB 9,800/ton. If the area is stable and has a rising momentum, look further at 10000. At 9800 yuan / ton, the upside momentum was insufficient, and it began to take profits. Depending on the condition of the disc and the technical trend, the trading volume can be rolled and gradually profitable. (5) Risk-to-reward ratio assessment: The expected risk-to-reward ratio is 3:1. 2. Arbitrage operation strategy Buy L1801 to throw L1805 Arrival strategy When the price difference between L1 month and L5 month is located at -100-(0) yuan/ton open position, buy L1 throw L5 exit strategy stop loss in equal proportion. If the closing price gap falls below -200 yuan/ton, the stop loss will be displayed. Loss: The risk is controlled within 5%. If the profit spreads as expected, it will rise back to 300 yuan / ton (average price) Of course, if the spread reaches 300 yuan / ton, there is still room for expansion under the cooperation of the fundamentals and technical aspects at that time, then you can continue to hold the second target of 500 yuan / ton, otherwise all hedges will close the position and profit from the vicinity of 300. Risk and benefit assessment Risk-to-benefit ratio: 1:3 (2) Risk warning 1. The prices of upstream crude oil and ethylene fell sharply, and their cost support weakened; 2. The newly added capacity of the device is put into operation and the operating rate of the device is maintained at a high level, and the supply pressure is increased; 3. The demand for basic plastics is less than expected. 4. The arbitrage plan adopts a bottom-up statistical analysis, whose analysis is based on historical trends, and the price may deviate from the conventional trend. 5. Due to the leverage of futures, the risk of futures market is large, and arbitrage is also the case. Risk control and capital control need to be strictly implemented. 6. The monetary policy continues to tighten. Ruida Futures Enter [Sina Finance and Economics Unit] Discussion The leather base is all there Pu Leather,Pu Leather Fabric,Embossed Pu Leather,Pu Fabric Leather WENZHOU JOVAN INTERNATIONAL COMMERCIAL , https://www.jovanleather.com